Life Insurance Guide Learn Term vs Whole Life Insurance

Selecting life insurance can be daunting. With over a half-dozen policy types, premium variations, and impenetrable terminology, it is easy to overspend on unnecessary coverage or purchase insufficient protection. This guide to life insurance is designed to demystify the process, assisting you in making informed, cost-effective decisions without missing out on peace of mind.

Among the initial planning steps, you'll find you have significant questions: How much insurance do I require? Term life or whole life insurance—what's best for me? Who provides the best life insurance for families at the lowest cost? And most importantly, how do you maintain protection within your means?

This is the complete guide that answers all those questions with practical advice and techniques so you can acquire the correct policy without spending more than you have to.

Learning the Fundamentals: What Is Life Insurance?

Essentially, life insurance is an agreement between you and the insurance company. You pay a monthly or annual premium, and in exchange, the company pays your designated beneficiaries a financial benefit when you die.

The purpose of life insurance is straightforward: it protects your loved ones from financial hardship. Whether it’s to help your family cover funeral expenses, bridge lost income, or leave a legacy of financial security for your children, making sure you have the proper coverage will provide financial peace of mind to your family.

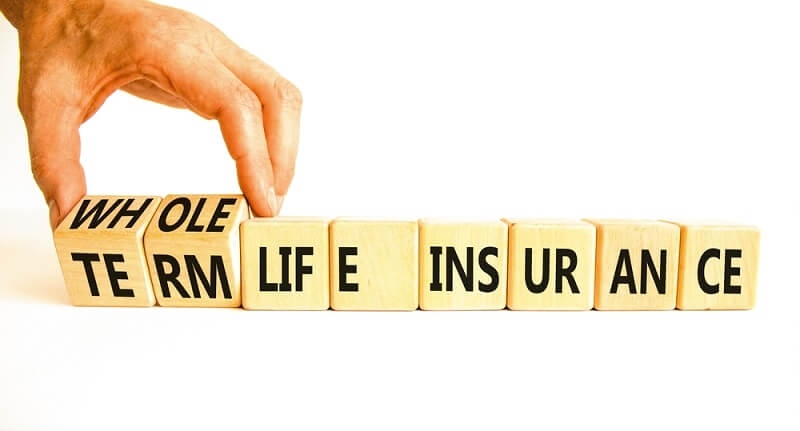

Term vs Whole Life Insurance: What’s Right for You?

One of the first decisions you will be faced with is term vs whole life insurance. Each serves a particular need and comes with its advantages and disadvantages.

Term Life Insurance

- Definition - provides coverage for a specified period, usually 10, 20, or 30 years.

- Best for - those who would like to have affordable life insurance.

Pros:

- Less expensive than permanent insurance policies.

- Allows some flexibility for your needs (mortgage, child's college tuition).

Cons:

- Does not have a cash value.

- Will cause you to have coverage until the end of the term.

Whole Life Insurance

- Definition: Permanent coverage which remains in effect for your whole life, as long as premiums are paid.

- Best for: Individuals who want lifetime protection and wealth-building aspects.

Pros:

- Accumulates cash value you can borrow against

- Stable premiums that never rise

Cons:

- More expensive premiums than term policies

- More complicated structure

Bottom line: If cost is your main priority, term life insurance could be the better buy. If you desire long-term wealth benefits and assured lifetime coverage, whole life insurance could work best for you.

How Much Life Insurance Do I Need?

This is one of the most frequent and essential questions. Purchasing too little coverage exposes your loved ones to financial risk, and purchasing too much can break your budget.

General Rule of Thumb

- Most advisors suggest that you buy coverage equal to 10–12 times your income per year.

For instance:

If your income is $60,000 per year, you might think about buying $600,000 to $720,000 in life insurance.

Considerations

- Existing Debts: Home mortgage, auto loans, credit card debt

- Upcoming Expenses: College education expenses for children, retirement expenses for spouse, medical expenses

- Living Costs: Length of time you wish to continue replacing income for relatives

By objectively considering these considerations, you can establish the proper balance of coverage without breaking the bank.

The Best Life Insurance for Families

When deciding on the best life insurance for families, consider your family's specific needs.

Why Families Need Coverage

- To replace the income of the main breadwinner

- To pay for childcare and household expenses

- To allow children to seek education without financial burden

Recommended Policy Types

- Term Life Insurance: Cost-effective coverage in years of high expense (raising children, mortgage payments).

- Whole Life Insurance: Best for families who desire generational wealth and lifelong protection.

Example Scenario

There is a family of four with two working parents. A term life insurance policy of 20 years may cover the family until the children graduate from college. If a parent dies, the payout prevents the family from going financially under.

Best life insurance for families maximizes affordability and duration of coverage.

Affordable Life Insurance: How to Save Without Losing Coverage

Life insurance doesn’t have to be expensive. Here are several ways to identify affordable life insurance coverage without sacrificing coverage:

- Select Term Not Whole Life: Term policies are approximately 60% less expensive.

- Purchase Early: Premiums are less at a young, healthy age.

- Shop and Compare Quotes: Look around to find the best rates via multiple providers.

- Bundle Policies: A few insurers provide a discount if you buy life insurance together with an auto or home policy.

- Stay Healthy: The cost of premiums for non-smokers and policyholders with healthy BMIs is significantly lower.

Common Mistakes to Avoid When Buying Life Insurance

Most buyers make costly mistakes that diminish the effect of their policies. Avoid the following errors:

- Underestimating Coverage Needs: Don't just consider burial costs: think of losing wages and expenses that will carry on long after.

- Overpaying for Whole Life Insurance: only pay for whole life insurance if you have established a need for permanent coverage—you will almost always be able to get a cheaper term policy.

- Not Reviewing Policies: As your family grows or debts are paid down, there will be changes in the needs of your family.,

- Relying upon employer coverage alone: Most employer coverage, if available, is insufficient coverage, and if you change jobs it is usually not transferable.

Comparing Providers: What to Look For

When comparing providers, don't shop based on price alone. Consider the following:

- Financial Strength Ratings: Select firms with excellent ratings (A or better).

- Customer Service: Dependable assistance is essential during claim settlement.

- Policy Flexibility: Seek out riders such as accidental death benefits, waiver of premium, or child coverage.

- Reputation: Look for reviews and complaint ratios to determine customer satisfaction.

How to Apply for Life Insurance

The application process may differ, but it generally includes:

- Get Quotes Online: Compare rates and policy features.

- Complete an Application: Provide personal, health, and financial information about yourself.

- Possible medical exam. You may have a blood test, a urine sample, and you will answer some health questions.

- Underwriting. The insurance company assesses your risk and sets your premium.

- Policy Approval: When you are accepted, you will start paying premiums, and then you will receive your policy.

Life Insurance for Unique Circumstances

Not everyone falls into the "normal" life insurance category. Here are some unique circumstances:

- Single Parents: Additional protection is likely important because kids rely on you alone.

- Stay-at-Home Parents: They may not generate an income, but their activity (childcare, home maintenance) is worth money.

- Business Owners: Coverage can be used to help with succession planning or to protect against business partners

- Seniors: Seniors may be a bit limited in their choice, but guaranteed issue life insurance will provide basic protection.

Evolving Your Life Insurance

Life evolves, so your insurance should evolve. Make a point to review your policy every few years or after a major life event. When you get married or divorced, purchase a home, have kids, deal with significant job changes, or approach retirement.

Tailoring coverage means you can guarantee your family is always at the right level of protection.

Final Thoughts: Make Wise Decisions without Breaking the Bank

Life insurance is not as difficult, complex, or expensive as it sounds. By understanding term vs whole life insurance, asking how much life insurance do I need, and looking for the best life insurance for families, you can finally have peace of mind without emptying your wallet.

This life insurance guide has provided you with enough information to confidently shop the market, compare policies, and have a reasonably priced life insurance coverage option to meet your needs.

Ensuring your family's financial future is likely one of the most important financial decisions you will ever make, so be diligent in comparing, researching, and selecting wisely.

This content was created by AI